Introduction to Supply and Demand

As I previously stated, "Everything you consume is influenced by supply and demand and impact prices of consumer goods and services within an economy." This relationship between supply and demand will balance out into an equilibrium with prices; when this equilibrium is reached, a perfect allocation of resources of production will occur. At this point, prices are perfectly set to the interest consumers and companies, and production will occur where they will produce neither too much nor too little product. Businesses use this as the mechanism determining product development and production.

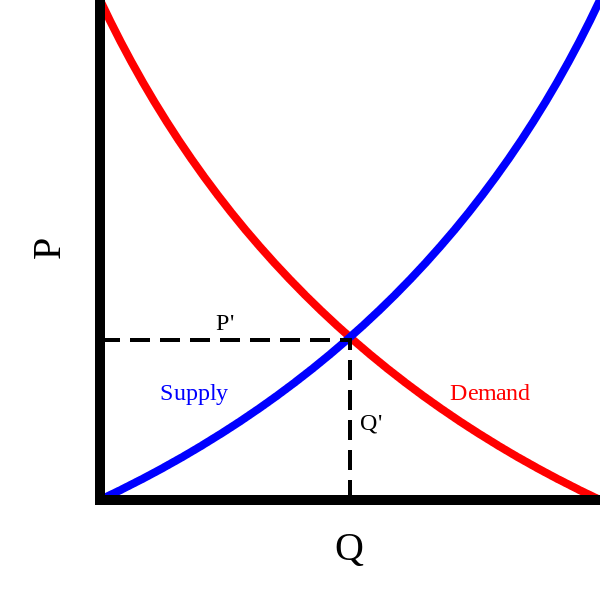

Consumers, then, dictate which products are produced and sold by creating the demand for companies to supply with goods and services. Companies study consumer behavior in an attempt to understand current and future demand. The capacity to produce enough supply to meet demand keeps prices low enough to entice consumers. In this sense, both supply and demand are equally important to economic vitality, and very important to learn. Below is a picture of a supply curve and demand curve with the equilibrium point being where the two curves cross.